About GAAP and tax adjustments

Related information

At the end of the fiscal year, companies reconcile their accounting for Generally Accepted Accounting Principles (compliance) and tax rules. As a result of these reconciliations, several adjustments are proposed for these organizations to be compliant.

GAAP and tax adjustments

It’s typical to post these adjustments without changing historical monthly amounts for the fiscal year to maintain the integrity of the operational reporting. Examples of these adjustments are depreciation, amortization, and tax liability.

You can do the following:

- Use GAAP and tax adjustment journals to post adjustments separately

- Report on the adjustments separately, or in combination with your actual books

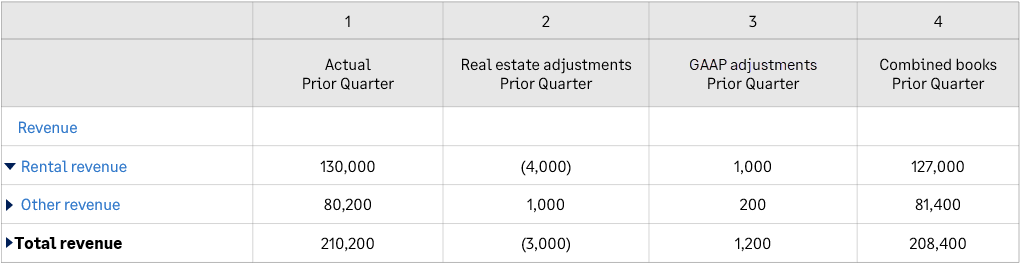

For example, the following financial report includes columns for adjustments that have been made—1 column for GAAP adjustments and another for adjustments entered in a user-defined book. The last column combines the Accrual book with the adjustments. Learn more about reporting on GAAP or tax books.

- Column 1: Accrual book

- Column 2: User-defined book; in this example, Real Estate book

- Column 3: GAAP book

- Column 4: Combined books; in this example, accrual + Real Estate + GAAP